As covered in our article on asset classes, bonds are a substantial subset of fixed-income assets. They produce higher returns than saving accounts and CDs (certificates of deposit), but lower returns than real estate and stocks. However, they do not come without jargon and terms that need explaining to the everyday investor. This is where we come in, to demystify the jargon and provide everything you need to know about them before buying in. So, what are bonds? let us jump in.

What are Bonds?

In general, investors should understand their investments well. Understanding what you invest in will naturally lead to better investment decisions. Bonds are securitised debt, which means that it is debt that is packaged up and issued to investors rather than financed by banks. It is one of the main ways of raising capital for companies and governments. Government bonds are issued by governments and corporate bonds are issued by…you get the point. The distinction does not matter as much as the credit risk, which we introduce next.

What is Credit Risk?

Investors usually take on risks expecting to be compensated for these risks. The higher the risks investors take, the higher the compensation they expect would be. Credit risk is the main type of risk investors take when investing in bonds and it’s the risk associated with lending money. The good thing for investors is that there are agencies with the sole purpose of assessing this risk, credit rating agencies (CRAs). The bad thing is that there are only 3 CRAs that monopolise the market and they have failed investors before during the ’08 financial crisis.

CRAs assign credit ratings to issuers of debt. This credit rating is akin to credit scores for consumers. The higher the rating, the more creditworthy the debt issuer is. There are 3 main CRAs that control 95% of the market: Moody’s, Standard & Poor, and Fitch.

The Credit Rating Scale

The scale differs slightly from one CRA to another. S&P and Fitch’s credit scale is AAA, AA, A, BBB, BB, B, CCC, CC, C, and D (High to low). Moody’s credit scale is Aaa, Aa, A, Baa, Ba, B, Caa, Ca, and C. The credit rating represents the probability of failure to repay the debt or the default probability of the borrower.

The creditworthiness of borrowers and the quality of their bonds are categorised mainly as investment-grade and speculative-grade. Investment-grade bonds are those with a minimum credit rating of BBB (S&P or Fitch) or Baa (Moody’s). Any bond with a lower credit rating is deemed speculative-grade, which promises a higher yield but is riskier. Note the word promises, because the advertised interest may never be paid if the borrower defaults.

Before We Go Any Further…The Jargon

Like any financial instrument, there are bond-related jargon, so we break down the key bond-related terms for you below:

- Maturity Date: This is the date when the bond matures and the borrower repays the principal back to investors.

- Face Value: This is the amount that will be repaid to investors on the maturity of the bond.

- Coupon/Coupon Rate: This is the interest/interest rate that investors receive from the borrower. It may be different than the yield for reasons that are explained below.

- Coupon Date: These are the dates when the borrower is scheduled to pay the coupon rate to investors.

- Issue Price: This is the price of the bond when it is first issued. This is usually the same as the face value, but may sometimes be lower, depending on bond type.

The Returns of Bonds

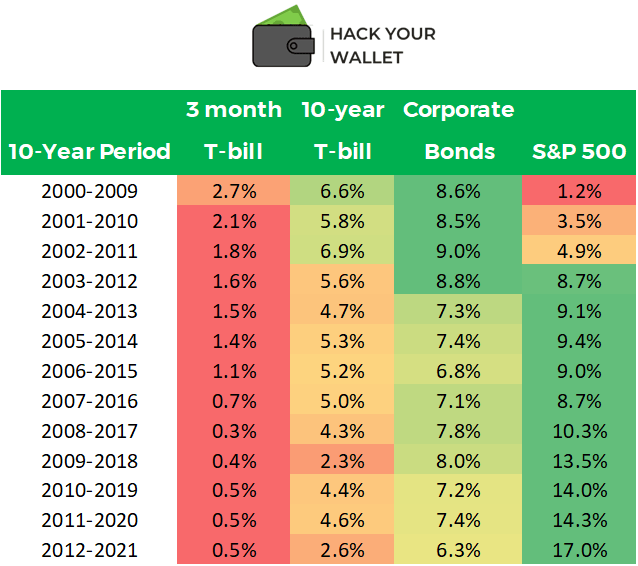

Now that we know all about CRAs and their credit ratings, how do we translate this to risk/return profile? It is not easy to answer but we try to provide some insight. The table below shows the average total returns over 10-year periods (2000 till 2021) for short-term treasury bonds (3-month T-bill), long-term treasury bonds, corporate bonds (Baa credit rating), and the largest 500 US companies (S&P 500). Total returns include the interest (dividends in the case of stocks) and the increase/decrease in the asset price. The returns are emphasised using a red-yellow-green colour scale.

The US issues bonds with different maturity dates, the earlier the maturity date, the lower the coupon rate. This is reflected above in the low average returns of 3-month treasury bills. What may come across as surprising, is the strong performance of corporate bonds relative to the stock market in the period 2000-2011. The underperformance of this specific period will be extensively explained in our article on the stock market. For now, it would suffice to revisit our article on opportunity cost for a reminder on average US stock market returns.

The Risks of Bonds

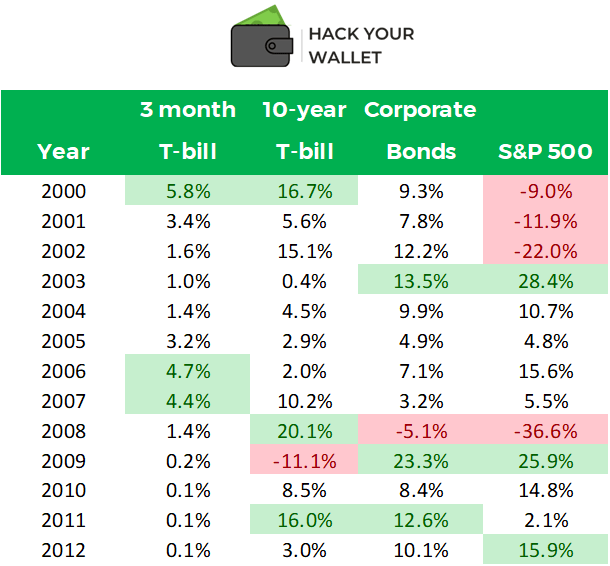

So we looked at average returns over 10 years, which tell us nothing about the level of risk associated with these investments. One way of looking at risk in finance is by assessing the variability in yearly returns relative to the long-term average. To do that, we present the yearly returns for the same assets above for the period 2000-2012. We could have gone all the way till 2021, but we believe this should be enough to illustrate the “variability” in returns. Extreme returns are highlighted in green and red.

As seen, the variability in returns is greatest with stocks and decreases for bonds. Also, bonds with shorter terms offer lower returns with lower volatility. This is expected due to the lower credit risk associated with short-term borrowing from the US government. However, it seems that bond returns have been trending downwards, which makes the assessment of bond returns difficult. The reason behind this trend is the undeniable correlation with interest rates.

Why Interest Rates Are So Important

We cannot discuss bond returns without mentioning interest rates and the impact they have. Central banks set the base interest rate. This is the interest rate commercial banks are charged for their borrowings from the central banks. Borrowing costs across the board are affected by changes in the base interest rate. Everything from mortgage rates to credit card rates is affected, including bonds. When interest rates are low, bond returns are low, and vice-versa. This is because when borrowing costs are suppressed by the central banks, the offered coupon rates reflect that. Also, when coupon rates are low, investors looking for income and decent returns are less keen on owning bonds, which further reduces the total return of bonds.

Interestingly, when interest rates are increased, bond prices go down and it is important to understand why. For that, the key concept of bond yield must be introduced.

Bond Yields

Most bonds are traded publicly on the financial markets, which means investors can buy newly issued bonds and sell them on to other investors well before maturity. The liquidity available in financial markets via market makers and other institutions naturally leads to volatility in the prices of bonds. Knowing that coupon rates are fixed but bond prices can and do change leads to the yield concept. The concept is fairly straightforward and presented below:

Bond Yield = Coupon/Bond Price x 100%

As usual, we shall demonstrate the concept with a few examples.

Example 1: Newly Issued Bond

Company A issues bonds in order to raise some capital for an acquisition. The offered coupon rate is 2.5% and the face value of each bond is £100 with a maturity date 10 years after issuance. John Doe decides to invest the minimum required investment for investors to buy in on issuance day, which is £1000.

Coupon = 2.5% x £100 = £2.5 annually per bond

Since John paid the Face Value of the bond, the yield and the coupon are the same.

Example 2: Publicly Traded Bonds

John decided to sell his bonds through his broker 1 year later and Jane ends up buying them. Company A has a high credit rating and the coupon rate they are offering is considered high compared to other investment-grade bonds. This leads to strong demand post-issuance and Jane ends up paying £105 for each bond. Since Jane paid more than the face value of the bond, the yield on her investment is different to the coupon rate.

Yield = Coupon/Bond Price = £2.5/£105 x 100% = 2.38%

It can be seen how the bonds will now yield less income relative to the initial investment for Jane, since she paid more for the bonds. But things get worse for Jane.

Example 3: Rising Interest Rates

Shortly after Jane invested in Company A’s bonds, the central bank raises interest rates to 3%. Because Company A pays only 2.5% on their bonds and newly issued bonds offer 3%+ coupon rates, demand drops. Jane is forced to sell her bonds at a loss, fearing further losses with further interest rate hikes. John considers investing again in Company A bonds which are now trading at £90, but first he calculates the yield to assess the investment.

Yield = £2.5/£90 x 100% = 2.78%

Figuring that the bonds would yield only 2.78% at the current price, which is still lower than the new base interest rate, John decides to look for another investment that yields higher returns.

Hopefully it is now clear why bond prices go down with interest rate hikes. Governments and companies will pay coupon rates closely linked to the base interest rate set by the central bank. Investors will quickly sell bonds in anticipation of, or in response to, interest rate increases. Before we wrap-up, there are different types of bonds that any bond investor needs to know.

Types of Bonds

- Zero-Coupon Bonds: These are bonds that offer no coupon payments! Yes, you read that right. Instead of paying interest, issuers of this type of bond issue it at a discount to its face value, so you end up paying £90 for a £100 repayment at maturity. Check out our article on Time Value of Money to judge this investment.

- Convertible Bonds: These bonds have an option to be converted to stocks at some point. Accrued interest can be and usually is paid in the form of additional stocks when converted.

- Callable Bonds: These bonds offer the borrower the option to “call-back” the bonds. This means that the borrower can decide to pay back the investors the principal and buy back the bonds.

- Puttable Bonds: While callable bonds give the borrower the option to buy back the bonds at any time, puttable bonds give investors the option to sell the bonds to the borrower at anytime. This makes puttable bonds more valuable.

- Islamic Bonds: Also known as Sukuk, these bonds are structured very differently to conventional bonds. They are usually asset based and tend to be difficult to access for retail investors. However, there are available funds nowadays that provide access to these fixed-income assets.

This Is Not All, But…

There you have it folks, everything you need to know about bonds. We answered the question what are bonds as comprehensively as we could. From their definition to their types, we covered the fundamentals of this popular fixed-income security. Although we covered all the fundamentals, there is more to learn about bonds. Mainly how to buy, sell and value different types of bonds. However, we at HYW are not big fans of bonds so we will only recommend Investopedia for further learning on the topic. In the meanwhile, you can stay up to date with our latest content if you subscribe to our weekly newsletter.

Subscribe to our newsletter!