Overspending is quite common, just ask your friends and family how often they stick to a budget. Matter of fact, you might be surprised to know that some don’t even have a budget. Many factors affect spending habits, credit cards enable a lifestyle beyond our means and capitalistic driven consumerism fuels consumption. Combining these factors with a lack of financial discipline and overspending without ending up indebted is the best-case scenario.

It could also be argued that the perception of having disposable income may be the culprit behind overspending. Regardless of the reasons, if you go over your budget, or don’t have one, zero-sum budgets are a powerful tool to develop financial discipline and avoid overspending.

What is a zero-sum budget?

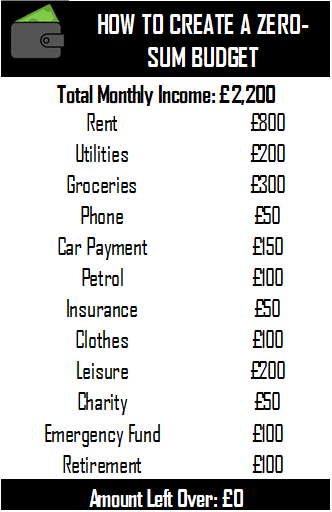

Popularised by You Need A Budget in 2005, zero-sum budgets are all about assigning every single penny of your income to an expense. This means every expense is accounted for and you are left with nothing at the end of the month. You might think “what about emergencies?”. Well, even emergencies are accounted for in a zero-sum budget using an emergency fund expense. The idea is that you put away money every month in an emergency fund whether you have an emergency or not. When emergencies do happen, you draw from your emergency fund.

How it works?

First, you need to know exactly how much income you earn. You can already see that this budgeting technique is not straight forward for people with variable income. The self-employed may prefer other budgeting techniques, but this could also work with slight modifications – we will glance at the “how” of this later in the article.

Second, you need a detailed list of expenses extracted from your last 3-6 bank statements. So detailed that it covers every single outgoing in a month. Even quarterly or yearly expenses must be included. A broad term such as savings or entertainment may not be good enough; break them down further. For example, I could further break down the leisure line item shown in the example above to Netflix subscription, eating out, and cinema. The more detailed the budget is, the better you can optimise your spending. You might find that you have 3/4 subscriptions to streaming services, which is a great opportunity to review your subscriptions/bills.

Finally, you need to allocate money to each of your expenses and ensure that the total sum is exactly equal to your income. If you have a surplus, then you can increase your leisure, clothing, or savings amounts as you see fit until you get to zero-sum. If you have a deficit, you need to review your expenses and cut spending somewhere.

The Keys to Avoiding Overspending

Theoretically speaking, this technique sounds sensible and easy. But in practice, it could get messy; an unforeseen additional charge here or a bill hike there will dent your budget. Here are a few tips and tricks to pull off the zero-sum budget technique, or any budget for that matter:

- Multiple bank accounts: This is an absolute must. You have to have different “wallets” for your various expenses. I use 3 bank accounts to make my budget work. I use different cards to pay for different types of expenses.

- Investment accounts: You need to keep your emergency fund and savings separate. I have an ISA (investment savings account) for my savings and a GIA (general investment account) for my emergency fund and yearly expenses. More on investing here.

- Direct debits and standing orders: Automate, automate and automate! Set direct debits for all your bills and to your ISA and GIA. Set up a standing order for your leisure allowance to go to your leisure account. If your spending is automated and expenses are calculated, there is little room for error. Bonus tip: outgoings automated on payday is the best way to minimise any surprises later in the month.

- Control your bills: Apply a spend cap on your phone bill. Overpay a little on your energy and water bills to stay in credit.

- Manage lifestyle inflation: Congratulations! You got that promotion at work and want to live it up a little larger? By all means, it is important to enjoy ourselves, but try not to get swept away. Overinflation of our lifestyles can easily make expenses spiral. Control which expenses you choose to increase and stick to it.

How does it compare to other techniques?

Budgeting is definitely for everyone, whether you have the discipline or not. However, zero-sum-based budgeting is not the only technique out there. See a summary of other techniques below and let us know if you’d like to know more about any of them.

- “Pay Yourself First” Budget: Dedicate a portion of your income to savings and you are free to spend the remainder as you choose. Very flexible and only works if you have plenty of disposable income. Even with high disposable income we would recommend the 50/30/20 budget over this.

- Envelope Budget: Divide cash into physical envelopes filled with the exact amount of money you can spend on that category. This is a bit like zero-sum budgeting in cash. Of course, keeping cash around comes with risk of burglary. We’d recommend zero-sum budget with a multiple debit/credit cards.

- 50/30/20 Budget: 50% of your income is for essentials, 30% is for personal expenses, and 20% goes towards savings. This is a fine approach but it definitely requires a high income; not everyone can afford all the essentials on just half their income.

- Value-Based Budget: Allocate the monthly budgets to your wants and needs based on your values. This is a thoughtful approach to budgeting. But it’ll also require some disposable income and arguably can be combined with the 50/30/20 budget technique.

What if my income varies?

You can still modify the zero-sum budget to make it work. You would build your budget starting with your essential expenses. Assuming that your minimum monthly income covers your essential expenses, you can then allocate proportions of disposable income to the remaining expenses. This would work very well in a spreadsheet, so let us know if you think it’ll be helpful and we will develop a template for free!

In Summary..

In summary, zero-sum budgets may seem boring and require some work to set up, but they definitely help avoid overspending. If you have a variable income, you may find other budgeting techniques easier to implement but we can still help you set it up.

Comments are closed.