Investment returns are surprisingly complex. One would have thought that it is quite straightforward to know what a good return is. But with a bunch of guaranteed returns thrown around on social media for a myriad of investments, we are here to bust myths. What is a good investment return? Let us dive in.

The risk-return complex

One could simply assume that a good investment return is a high return, but it is not that simple. Firstly, high returns are subjective, reasonable people are quite satisfied with 10% a year, while others would be disappointed with only a 100% return. Secondly, the risk profile of an investment that returns a couple of percentage points a year is very different than one that returns double-digit returns. For that, we need to introduce the concept of risk-free returns. This concept offers a brilliant benchmark to measure and judge investment returns, and in turn, the investments themselves.

What is the Risk-Free Return?

Risk free returns have two key characteristics:

- No default risk i.e. no credit risk

- No reinvestment risk

We have introduced credit risk in our article on bonds. As a quick reminder, it is the risk of failing to pay the borrowed money back to investors. Reinvestment risk means you do not have to cash out and reinvest your capital at some point to achieve the return. US government bonds usually meet both criteria. With the dominance of US dollar as a reserve currency comes a demand for US dollar-denominated debt and unparalleled capability of the US government to service that debt. Additionally, US government bonds come in various maturity dates, which is why these bonds do not have a reinvestment risk.

How to work out the risk-free return?

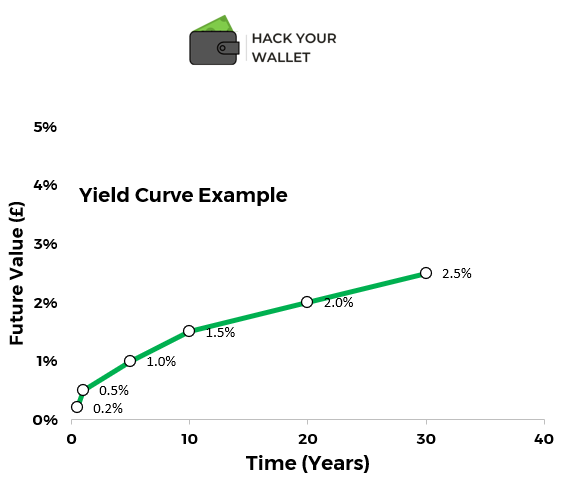

To work out the risk-free return, one must start with the investment time horizon. Essentially, how much time you can spare that money? If you need the money in 1 month, then your investment time horizon is 1 month. Risk-free returns decrease with the investment time horizon. Once the time horizon is defined, finding the risk-free rate is as easy as looking at a chart or googling a sentence. The chart in question is the US yield curve. The yield curve shows the return (yield) of US bonds held to maturity with different maturity dates. An example is shown below for a normal yield curve.

The normal yield curve is the expected shape of the yield curve in normal times. In times of recession or economic distress, interesting things might happen to the yield curve. However, this falls outside the scope of the article. In normal times, investors demand higher returns on longer maturity dates. While in times of economic distress or uncertainty, investors may want higher returns in the short term. This is a phenomenon known as yield curve inversion.

Someone might think that you can be better off investing in shorter-term bonds and reinvesting the capital at the end of the bond term. However, this introduces reinvestment risk. To ensure the return is risk-free, one must consider the yield associated with his or her investment time-horizon.

The US government does not actually call all their issued debt bonds, even though they are technically bonds. For completeness, the chosen US government nomenclature for their issued debt is summarised below:

- All bonds maturing in 52-weeks (1 year) or less are called treasury bills or T-bills.

- All bonds with maturity between 1 year and 10 years are called treasury notes or T-notes.

- Bonds with maturity beyond 10 years are called treasury bonds. Note that these bonds have either 20 or 30 year maturity dates.

To find the relevant rate, TreasuryDirect, Yahoo Finance, or Financial Times can be used.

So Risk-Free Returns Are Good Returns?

Not necessarily. Risk-free returns offer investors a benchmark to judge other investments. It also offers a good base reference to catch out scammers, ponzi-schemes and unsustainable crypto projects. If an investment promises guaranteed returns that are well above the risk-free return, be assured that this investment is either a scam or has hidden unadvertised risks. With that said, let us look at some of the most common risks that contribute to higher returns.

Credit Default Risk

With the exception of the largest and most developed economies, all government and corporate issued bonds carry some default risk. This risk is captured in the yield of the bond, which will be higher than the risk-free return. The difference between the risk-free return and the return of the bond in question is the credit default spread. We mentioned before that this the most relevant risk to bond investors, and it explains why a small company with a weak balance sheet will issue bonds that yield 10% above the risk-free rate while Microsoft will only pay 1% above the risk-free rate.

Equity Risk(s)

These are risks associated with investing in stocks. There are a few and we will not get into any of them in detail, but it is vital that investors know they exist. Broadly speaking, investing in stocks comes with two main types of risk, defined as follows:

- Compensated Risk: These are risks that the investors can expect to be compensated for. There are a few compensated risks, but the most relevant one to the average investor is market risk. Market risk is associated with investing in the stock market. It captures all external factors that may affect the return of the market as a whole, such as economic or geopolitical risks.

- Uncompensated Risks: These are additional risks that are unique to a single company, sector, or country. Investors should not expect to be compensated for taking on more uncompensated risks. This is not to say that these risks will not affect your returns. In fact, the concept of risk-adjusted returns is specifically developed to capture the level of uncompensated risks in a portfolio.

In Conclusion

So what is a good investment return? Well, they vary from one person to another. The time horizon and appetite for risk play an important role in determining what constitutes a good return. Risk-free returns offer a great benchmark for assessing investments. Any investment that offers returns in excess of the risk-free return must carry some risks. It is important for investors to be aware of these risks and allocate their capital accordingly. If you want to learn more about risks when investing, join our weekly newsletter below for regular updates.

Subscribe to our newsletter!