The most important concept in finance is probably the concept of time value of money (TVM). It is the first principle behind the concepts of Present Value (PV) and Net Present Value (NPV). It is why loans carry interest and capital is invested. Once these concepts are broken down, you will see why you should never keep a lot of cash around.

What is TVM?

We briefly introduced the concept of time value of money (TVM) before when we discussed inflation. We said, and we quote:

The fact that purchasing power decreases over time and that your cash is worth less in the future leads to the important concept of time value of money (TVM). In essence, TVM states that one dollar today is worth more than one dollar tomorrow.

Hack Your Wallet, “How Inflation Damages Your Finances and 7 Ways to Beat It”

That is it folks. That is all you need to know about TVM. Cash loses value over time due to inflation so your money is worth more now than later. There is also an opportunity cost associated with delaying cash flows, there are missed returns on cash received later. Despite its simplicity, the implications on financial decision making are serious. How you finance every purchase is relevant. It becomes clearer when TVM is used in the concept of present value (PV) and Future Value (FV).

What Is PV and FV?

When we claim that money has a time value, then ideally we need some way of calculating that money’s value in the future (Future Value). For cash flows expected in the future, we would like to calculate the value of that money in the present (Present Value). In both cases you need two variables, a rate of return and number of years. We will get a bit more technical momentarily but please bear with us, you are set to revolutionise the way your perceive money.

Is This Important? I Don’t Work in Finance

This is not just important, this is essential. Thinking about the time value of money and being able to work out the present value or future value is the skill that will take you to the next level financially. You’d be able to scrutinise investment returns, appreciate good use of debt and make the best possible financial decisions. You will be able to see benefit where others, intuitively, see otherwise. Best of all, it is not even that complicated. So let us get started.

Future Value (FV) Calculation

FV calculations are essentially applying the compound interest formula we all learned in Maths class. If your money is invested with an annual rate of return, your money is set to compound. Compounding is powerful because it has a snowballing effect that leads to exponential gains over the long term. The FV formula is shown below.

Future Value = Present Value x (1 + Rate of Return)number of years

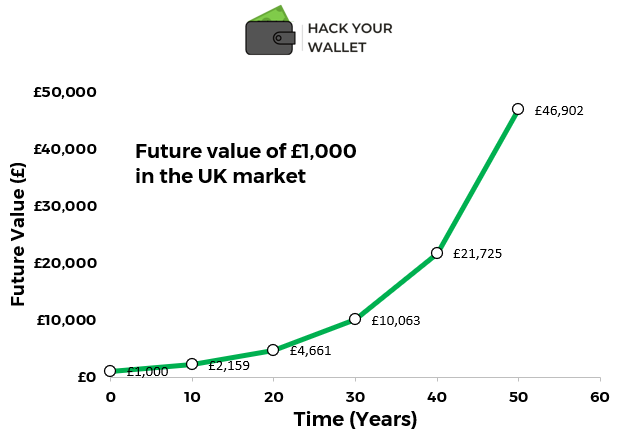

You can see how this formula can be easily used in a calculator. We mentioned in our article on opportunity cost that the average return of the stock market has been statistically guaranteed over 10-year periods in the past. This means that for every 10 year period for more than a century (that is more than 90 10-year periods!), the UK stock market returned 8% to investors per year. Let us use that as our first example.

Example 1: £1,000 in UK stocks

How much money should you expect if you invest 1k in UK stocks for 10 years? Let us plug the numbers in the formula and see:

Future Value (after 10 years) = £1000 x (1 + 0.08)10 = £2158.9

You can see how the money more than doubled. But to digest the power of compounding over time, let us look at longer holding periods.

- 20 years: 1k becomes 4.6k

- 30 years: 1k becomes 10k

- 40 years: 1k becomes 21.7k

To visualise the trend, we show the change in the value of 1k over time below. Logarithmic increase in value with a doubling rate of approximately 10 years.

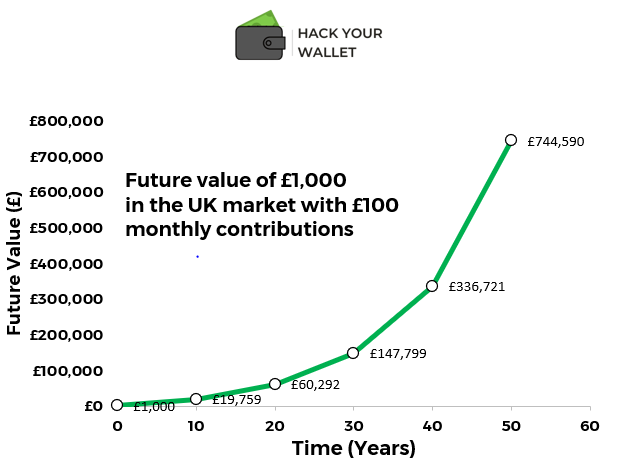

Example 2: £1,000 initial investment and £100 monthly contribution

Assuming that not only do you invest 1k in the UK market, but you also invest £100 every month, or 1.2k a year, how does this affect the future value? This calculation may require a spreadsheet but we did the maths and the numbers are mind blowing. The snowballing effect of that £100 boosts the returns significantly, as summarised below:

- After 10 years, you would have invested £13,000 and have a future value of £19,759. Not bad, but you better wait because

- After 20 years, you have put in £25,000 and have a future value of £60,292. Much better returns. The more you wait though, the more you gain.

Try Our Future Value Calculator

You can quickly calculate the future value of your savings using our handy calculator below. Just be careful about the rate of return you use. Good returns are not as easy as one might think.

What About Present Value?

So we have discussed how one could work out the future value, given the value of money now. But what if we need the present value of money we will receive in the future? Simple, using the same formula above. Rearranging the formula above for present value yields the following:

Present Value = Future Value/(1 + Rate of Return)number of years

The formula shown above is the foundation of Net Present Value (NPV) calculations, Discounted Cash Flow (DCF) valuations, commercial real estate valuations and even actuarial calculations (to work out your insurance premiums). Out of these, which ones are important? NPV calculations are really essential for business owners and entrepreneurs to evaluate projects and/or investments in the business. DCF is potentially the most important valuation techniques for companies, and we will cover this in further detail in our investing section. If it is a cash-generating asset, PV can help valuing it so that you don’t end up overpaying.

Do I Also Use Market Returns Here?

Not really. The idea of the present value is that this future cash flow will be worth less than money paid now because of two factors:

- Inflation. £100 in one year time will buy less goods than today. Note that the nominal value of cash does not change, but it is the price of goods and services that goes up.

- Opportunity cost. If you had been paid this £100 now, you would have invested and made some return. So this cost also needs to be captured in estimating the PV of the £100. We have established in our post on opportunity cost that usually, stock market returns are our best investment return.

Therefore, we like to use stock market returns in our present value calculations. But you can also use the returns of the best available investment to you.

Example 1: Present Value of £1,000 in 1 year time

Using a nominal return of 8% and £1,000 to be received in 1 year time, the present value can be calculated as follows:

Present Value = £1,000/(1+0.08) = £926

Knowing that a £1,000 in 1 year time is really worth £926 in today’s money, you can insist to get paid earlier or make necessary adjustments to make up for the lost £74!

Example 2: Present Value of £1,000 in 2 year time

Using a nominal return of 8% and £1,000 to be received in 2 year time, the present value can be calculated as follows:

Present Value = £1,000/(1+0.08)2 = £857

It can be seen how money can lose value if payments are deferred to the far future. Just like FV compounded logarithmically, PV will lose value logarithmically. This is why holding cash in savings is detrimental.

So How Does All of This Affect My Finances?

In a number of ways really. See the list below:

- Saving for a long-term goal: If you are saving for a house deposit, this may take a few years. Invest your savings, you are losing to inflation and missing on returns.

- Making large cash purchases: Making large purchases in cash when cheap credit is available does not make sense. You can invest the cash now and pay for your car/furniture/engagement ring using future cash flows, which we all now know, are worth less.

- Making Investments: Investing in stocks, real estate or business assets should be informed by present value calculations. We will explore these further in our investing section so subscribe to get first access.

In Summary

Time value of money is a key concept in finance, and your finances are no less important than corporate finance. Treat your cash like the king it is and make sure you are not missing out on cheap credit or investment returns. We explore how to calculate the future value of investments and the present value of future cash flows. So you are equipped with the foundational knowledge to start making better financial decisions.

Subscribe to our newsletter!